Search

Search

Previous Menu

Previous Menu

-jpg.jpeg?width=312&height=170&name=04_09_26_auto_loan_header%20(2)-jpg.jpeg)

.webp?width=300&height=169&name=GettyImages-2169016298%20(1).webp)

Tap into Your Home's Equity

Receive a lump sum payment to make the impossible possible.

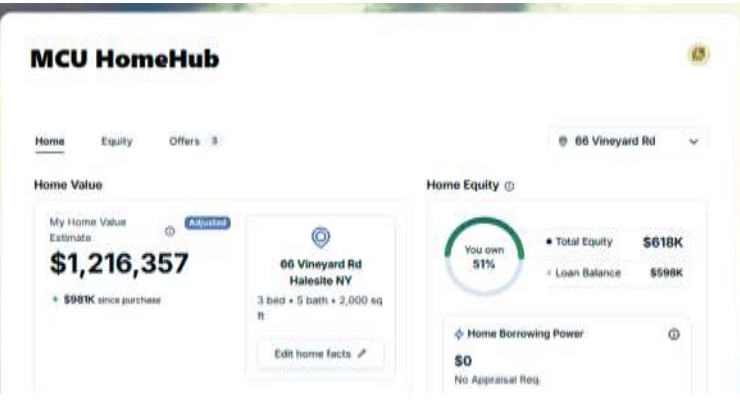

MCU HomeHub

Your home may be your most valuable asset. MCU HomeHub gives you a personalized view of your home's estimated value and available equity—right inside your digital banking app. No application needed.

Access MCU HomeHub

What you can do

Track your home's value

See your home's estimated value and get alerts when it shifts with the market.

Understand your equity

See how much equity you've built and your home borrowing power—no appraisal required.

Explore personalized offers

Get tailored HELOC and Home Equity suggestions based on your actual home value and profile.

How to Access MCU HomeHub

-

Log in to digital banking to check if you have been already automatically enrolled.

-

If not, provide your name and address to enroll.

-

Navigate to Services & Support

-

Select MCU HomeHub

Check Out Other MCU Home Equity Loan Solutions and Choose What’s Best For You!

Home Equity Line of Credit (HELOC)

Choose to spend as much or as little as you need with a variable, revolving Home Equity Line of Credit (HELOC). Like a credit card, you’ll be approved for more borrowing as you make payments toward your outstanding balance.

Home Improvement Loans

The Heroes Home Improvement Loan is designed to make home improvement projects more accessible and affordable—helping homeowners transform their living spaces with flexible loan terms, low fixed interest rates, and access to up to $50,000 in funds.

Get Expert Support, When You Need It

Connect with our home lending team for personalized support.

.jpeg)

.jpg)